What We Mean by Development Ecosystem Strategy and Why It Changes Everything

A destination is the system that determines whether assets such as heritage sites, festivals, national parks or even a resort generates sustained economic value.

This distinction is where our work at Red Clay begins.

Most conversations about tourism development in Africa start with attractions, arrival numbers, and hotel beds. These are reasonable things to measure, but they are outputs of a functioning system, not the system itself. When they become the primary focus of strategy, the result is investment that underperforms, infrastructure that sits underutilised, and tourism growth that is narrower and more fragile than it needs to be.

The pattern is consistent. A new hotel opens in an area with unmotorable roads, an underskilled hospitality workforce, and no coherent destination brand. Operations run below capacity. The supply chain imports rather than sources locally. The economic multiplier (the ripple of spending that should move through the local economy) leaks out rather than circulates. What is happening? The attraction exists, the investment arrived, but the ecosystem was not there to receive it.

Development ecosystem strategy addresses the conditions.

It works across five interconnected dimensions:

connectivity, which determines whether a destination can be reached at competitive cost;

hospitality capacity, which determines whether the accommodation and services infrastructure can support visitor demand;

workforce readiness, which determines whether the skills exist locally to deliver quality experiences;

safety and governance, which shapes the risk perception that drives investor and visitor behaviour;

and brand and reputation, which determines how a destination is understood and evaluated by the people whose decisions matter most.

In the ecosystem, no single dimension works in isolation. A destination with excellent connectivity but weak workforce readiness will attract visitors it cannot serve well. Strong hospitality stock without brand clarity is invisible to the investors and travelers most likely to value what it offers. A destination with all five dimensions functioning coherently becomes a place where investment and development decisions are easier to make, returns are more predictable, and tourism generates economic value that extends well beyond the sector itself.

This is what investment readiness actually means. This readiness goes beyond a marketing campaign or the development of a masterplan. It requires a system in which the conditions for sustained economic activity exist and are visible to capital. This is why we describe our work as development ecosystem strategy rather than tourism consultancy.

Tourism consultancy produces recommendations for the tourism sector. Development ecosystem strategy produces the conditions for a destination’s economy to work, over the long-term. Tourism is the vehicle, the sector through which connectivity, capacity, workforce, safety, and reputation are built and tested. But the question we bring to every engagement goes beyond how to improve visitor numbers. It is how do we make this place more competitive, more resilient, and more worth investing in, for residents, for businesses, and for the institutions that allocate capital across the continent?

Africa has numerous destinations worth investing in but the ecosystem infrastructure that makes these destinations valuable and accessible for investment and development is missing.

In February 2026, two Nigerian states made consequential decisions about how to develop their tourism economies. One committed ₦20 billion to runway refurbishment and acquired a 60-seat aircraft. The other approved a 10-year community-centred masterplan built around existing heritage assets and local ownership of tourism revenues. Both governments believe they are investing in the future. The evidence suggests they are not making equivalent bets.

This edition examines those two choices and presents what Ethiopia’s 15 per cent tourism growth in 2025 reveals about which development philosophy is more likely to produce durable returns. It also considers what Italy’s wine tourism sector, expanding even as global wine consumption declines, tells us about the economic logic of experience-led development in African agricultural regions.

The Infrastructure Trap: Two Theories of Development in Nigeria

Ekiti State’s Executive Council approved a Tourism Policy and 10-year Tourism Development Master Plan in February, establishing governance frameworks for sustainable tourism through 2035. The plan positions Ekiti as a heritage and nature-based tourism destination for Nigeria and West Africa, with communities structured as primary owners and beneficiaries of tourism revenues. Here, development builds from existing assets: Ikogosi Warm Springs, hill stations, sacred groves, and cultural festivals, rather than creating new infrastructure from scratch.

The timing reflects a deliberate reading of where international demand is moving. Travellers are shifting away from crowded, homogenised destinations toward authentic cultural experiences, nature-based activities, and wellness-oriented travel. Ekiti’s masterplan positions the state into that shift. Community-based models also distribute economic benefits more broadly, with value circulating through local populations rather than concentrating with external operators.

Ebonyi State is making a different calculation. The state has committed ₦20 billion to runway refurbishment and airport upgrades, acquired a 60-seat aircraft, and is awaiting regulatory approval for airline operations. The stated objectives include improved regional connectivity, stronger trade logistics, and increased investment in Abakaliki. These follow a familiar infrastructure-first logic: build the access, and economic activity follows.

The challenge is that airport viability depends on passenger volume thresholds that small regional airports rarely achieve without sustained subsidy. Research on regional airports demonstrates that facilities handling fewer than 200,000 passengers annually consistently struggle to cover operating costs, typically requiring subsidies ranging from US$150,000 to US$9 million annually, depending on size and services. Efficiently operated small regional airports require approximately 166,000 passengers annually to break even. This threshold demands a credible catchment analysis, documented competition assessment from neighbouring state airports, and realistic projections of business and leisure travel demand.

Ikogosi Warm Springs Resort is one of the many tourist attractions Ekiti State has to offer in their heritage tourism development masterplan

Image Credit: Desmond Okon/TheCable

Airports are also among the most energy-intensive commercial buildings in existence. Maintenance alone can consume up to 20 per cent of total operating budgets. The ₦20 billion runway investment comes to approximately US$13–14 million. This is a credible capital commitment. But the long-term question is whether the demand exists to justify the ongoing operational cost, beyond the initial construction cost.

The opportunity cost framing sharpens the decision. Comparable public investment could alternatively support a portfolio of heritage site restoration, rural-urban road linkages, hospitality workforce training, community tourism infrastructure, and destination marketing.

These alternatives distribute economic benefits across multiple communities and build the ecosystem conditions that determine whether any infrastructure investment, including airports, performs over time.

Ekiti’s model and Ebonyi’s model both represent legitimate development philosophies. But their risk profiles are not equivalent. Ekiti builds from assets that already exist and cannot easily become liabilities. Ebonyi has committed to infrastructure that requires sustained demand to justify its costs, and that demand does not yet exist at the required scale.

Ebonyi airport: significant public capital committed to runway and aircraft acquisition. The operational sustainability case remains to be made.

Image Credit: Nairametrics

What Ethiopia Got Right

Africa recorded 8 per cent growth in international arrivals in 2025, the strongest performance of any region globally. Within that, Ethiopia posted 15 per cent growth. This growth came from Lalibela, Gondar, the Simien Mountains, and the Omo Valley, existing assets that have been made more accessible. With improved stability following the Tigray conflict, resumed northern flights, better site interpretation, and targeted marketing to travellers who were already looking for exactly what Ethiopia had, Ethiopia’s tourism development trajectory shows what is possible when working with existing assets.

The demand pattern is significant. Younger travellers in particular are seeking immersive experiences at cultural and natural heritage sites such as the rock-hewn churches of Lalibela, the castles of Gondar, and the cultural landscapes of the Omo Valley. This reflects a broader shift away from overcrowded, homogenised destinations like Bali, Barcelona, and Venice toward places that offer what those destinations have lost: uncrowded access, cultural depth, and landscapes that have not been managed into predictability.

This growth trajectory carries direct implications for other African destinations. Secondary cities, rural areas, heritage sites, and natural landscapes across the continent possess similar latent potential. The formula, including asset identification, thoughtful access design, strategic branding scaled to realistic visitor volumes, requires considerably less capital than airports or convention centres, and generates returns that are more distributed and more durable.

Forest lodges, community-run heritage sites, themed village experiences, seasonal festivals, and adventure tourism offerings can attract high-value travellers while requiring modest capital. Some examples include Arusha, positioned as a gateway to the northern safari circuits and Kilimanjaro; the Kivu region in Rwanda positioned for lake tourism, coffee experiences, and mountain gorillas; and hillside destinations across the continent suitable for hiking and nature-based lodges. Africa’s competitive advantage in tourism is precisely what mature markets lack. Ethiopia’s numbers are proof that this advantage, properly presented and accessible, generates sustained demand.

Lalibela, a UNESCO World Heritage site in Ethiopia’s Amhara region, is a 12th-century holy city famous for 11 monolithic, rock-hewn churches carved from solid stone by King Lalibela

Image Credit: Andrew Hardin-White/Expedia

Growing Grapes to Build Economies: The Experiential Revenue Model

The global wine tourism market reached $46.5 billion in 2024, growing at a projected compound annual rate of 12.9 per cent. This goes against the paradox that global wine consumption has reached historic lows. Italy’s wine regions illustrate how this is possible. Wineries investing in tourism infrastructure, digital booking systems, and sustainable practices report asset growth exceeding 25 per cent from 2019 to 2024. Community economic impact exceeds €150 per visitor, with spending supporting agriculture, dining, retail, and hospitality services across the regional economy.

The structural lesson here is what happens when a traditional agricultural sector pivots to experiential revenue amid shifting commodity market conditions. The product becomes the experience of production itself, the vineyard tour, the harvest, the tasting, the landscape.

This logic applies directly to African agricultural regions with tourism potential. South Africa’s established wine regions in Stellenbosch, Franschhoek, and Paarl already demonstrate the model. Systematic expansion, by extending seasonal programming, developing integrated culinary and wellness packages, and improving international outreach, could materially increase visitor spending and stay duration.

Less examined is the potential of Africa’s high-altitude grape-growing areas. Jos Plateau in Plateau State, Nigeria supports abundant grape cultivation due to cool temperatures and suitable terrain. Ethiopia’s highlands and Kenya’s high-altitude regions share these characteristics. In February, Plateau State Government and UNDP hosted a three-day Tourism Master Plan Workshop examining natural attractions, cultural heritage, festivals, hospitality infrastructure, and policy frameworks. The integration of wine tourism into that planning process could diversify agricultural revenue while complementing heritage and nature tourism, creating year-round programming that reduces seasonal dependence and strengthens direct sales channels for local agricultural producers.

The Italian case demonstrates that experiential revenue can sustain an agricultural sector even when its primary commodity market contracts. For African regions with cultivation potential, the strategic opportunity is to develop that experiential layer before commodity market forces the pivot towards building tourism infrastructure while agricultural revenues are still stable, rather than as a response to their decline.

What These Developments Tell Us

The cases in this edition share a structural argument. Tourism development that builds from existing assets, whether cultural, natural or agricultural, and scales infrastructure to realistic demand generates more durable returns and distributes economic value more broadly than infrastructure-first approaches premised on demand that does not yet exist.

Ethiopia’s growth validates this, and Ekiti’s masterplan is designed around it. Italy’s expansion of wine tourism demonstrates this in a different sector. The common thread is the importance of sequencing: get the ecosystem conditions right first, then invest in infrastructure to meet demand.

Ebonyi’s airport may yet prove viable. But in this case, the burden of proof lies with a documented passenger demand analysis, a credible operational cost model, and an honest accounting of what the same capital could alternatively build. That analysis, if it exists, should be made public. Infrastructure decisions of this scale, made without such analysis, carry risks that extend well beyond the aviation sector.

December 2025 produced three developments that, read separately, each tell a partial story. Read together, they raise a single question that cuts across all of them: when tourism growth arrives in Africa, who captures it, and who absorbs its costs?

In Lagos, sections of Makoko were demolished under urban renewal justifications, displacing thousands of residents without adequate resettlement. In East and Southern Africa, domestic travelers quietly outperformed international markets in revenue contribution. And globally, cultural tourism continued its evolution from passive observation toward immersive participation, driven by demand that Africa is positioned to serve but has not yet systematically packaged.

These stories are three expressions of the same underlying challenge: Africa’s tourism growth is accelerating, but the systems designed to distribute its benefits and manage its costs remain underdeveloped.

The City and the Waterfront: What Makoko Reveals About Urban Tourism Strategy

Between December 2025 and early January 2026, targeted sections of Makoko, the riverine community along the Lagos Lagoon on mainland Lagos, were demolished. Thousands of residents were displaced. Civil society groups argued the demolitions violated international human rights standards. The government cited public safety risks from power lines. Whatever the legal justification, the outcome is consistent with a pattern that urban development research documents across rapidly urbanising cities: forced evictions rarely resolve the structural conditions that produce informal settlements. They merely relocate them.

Lagos faces a choice: treat waterfront communities as obstacles to development, or as permanent parts of the city with economic and cultural value that formal planning has not yet learned to capture.

While the rest of the world engaged in the December festivities, Makoko, a riverine community on the shores of Lagos Mainland, had sections targeted for demolition.

Image Credit: New York Times (Photography by Taiwo Aina)

Slum dynamics persist because they emerge from structural factors that include rural-urban migration driven by economic opportunity, insufficient affordable housing, weak land tenure, and informal labour markets that absorb workers essential to urban economies. When demolition proceeds without parallel provision of affordable housing, land tenure reform, or livelihood planning, the phenomenon surfaces in another part of the city within years.

The instructive comparisons are not hypothetical. Rio de Janeiro’s Favela-Bairro programme, implemented between 1994 and 2008, installed basic infrastructure; water, sanitation, electricity; within favelas. Land tenure was formalized and community centres and healthcare facilities were built within settlements. Some favelas in Rio’s South Zone, including Rocinha and Vidigal, subsequently developed tourism economies: guided tours, community-led cultural experiences, small hospitality ventures, and short-term rentals generating income that stayed, at least partially, within the community. Benefits are uneven and not all revenues remain local. But the model demonstrates that informal waterfront settlements can generate economic value when planned for rather than periodically cleared.

A picture of the favelas in Rio de Janeiro, Brazil

Image Credit: Where in Rio and Beyond

Benin’s Ganvié offers a different register. Built on stilts over Lake Nokoué, home to approximately 20,000 residents and now on UNESCO’s Tentative List of World Heritage Sites, Ganvié demonstrates how a water-based settlement can evolve into a cultural heritage destination while remaining a functioning community. Fishing and local trade remain central to daily life, while tourism provides supplementary income. The settlement faces infrastructure and environmental pressures such as water quality, structural maintenance and sanitation, but it has been planned for, rather than cleared.

Makoko’s viability as a comparable destination depends on whether Lagos is willing to make the investment that transformation requires: formalised tenure, basic infrastructure, environmental management, and a planning framework that incorporates rather than periodically removes. Without these, demolition produces visible action without durable change. Residents may relocate to equally vulnerable sites but the underlying housing demand remains unresolved and the structural pressures will resurface elsewhere in the city.

Lagos promotes creativity, tourism, and lifestyle branding. It has not yet decided whether the communities that define its waterfront character belong in that story.

A hotel stilt building in Ganvié, Benin. Ganvié formalized its informal floating village community and was listed on UNESCO’s Tentative World Heritage List. Can Lagos do the same for Makoko?

Image Credit: Beata Tabak/ArchDaily

The Data That Changes the Argument: Africa’s Domestic Tourism Revenue

Kenya’s national parks recorded over 313,000 visitors in December 2025. Domestic tourists accounted for 231,000 of them, nearly three times the 82,500 international visitors. The Kenya Wildlife Service’s framing was deliberate: local travellers form the backbone of the country’s tourism economy.

Across Africa’s largest tourism markets, the revenue data contradicts the dominant policy assumption that international arrivals are the primary engine of tourism income.

Sources: WTTC Economic Impact Reports, Ghana Tourism Authority, Tanzania Tourism Sector Survey Reports, OECD Tourism Trends and Policies 2024, Ministry of Natural Resources and Tourism Statistical Bulletin

In South Africa, domestic tourism spending reached approximately R430 billion in 2024, nearly four times the R116.5 billion generated by international visitors. In Kenya, domestic spending exceeded international receipts by more than 80 per cent. In Nigeria, the gap is more pronounced still: domestic tourism generated ₦5.35 trillion against ₦655 billion from international arrivals, a ratio of more than 8:1.

The picture inverts in North Africa. Egypt’s international tourism generated EGP 726.9 billion against EGP 449.9 billion in domestic spending. Morocco follows a comparable structure, with infrastructure, marketing, and connectivity heavily oriented toward European and regional international markets. Both countries have built tourism economies that perform well under stable global conditions and contract sharply when conditions shift. Morocco’s international receipts fell by more than 50 per cent in 2020. The structural exposure is documented and consistent.

The assumption that international arrivals are Africa’s primary tourism revenue engine is not supported by the data from the continent’s largest markets. In several of them, it has not been true for years.

What the data reveals is an underinvestment gap. Countries that built domestic tourism infrastructure with accessible pricing, internal mobility systems, year-round programming for local audiences, have developed internal markets that compete with or exceed international receipts. Yet tourism policy across much of the continent remains disproportionately focused on attracting foreign visitors through international branding and marketing campaigns aimed at European and North American source markets.

The strategic implication is to stop treating domestic tourism as fallback revenue and recognise it as the primary base it already is in several of Africa’s most significant tourism economies. Building this foundation requires sustained investment in internal mobility, accessible pricing that enables broader middle-class participation, and year-round product development that gives domestic travellers reasons to move within their own countries throughout the year.

Culture as Participation: The Conversion Gap Africa Has Not Yet Closed

China recorded 5.6 billion domestic trips and nearly 1.5 billion museum visits in 2024. Cultural tourism products such as heritage workshops, guided tours, culinary experiences, and living culture encounters surged in 2025 with double-digit growth in visitor orders and ticket sales.

The demand comes from travellers seeking cooking classes, calligraphy workshops, tea ceremonies, traditional clothing experiences, and homestays. These travellers desire hands-on engagement with heritage and daily life.

This pattern is not China-specific. UN Tourism estimates approximately 40 per cent of all international tourists now travel primarily to experience culture. Kayak’s 2026 travel research signals the same direction among younger travellers: small towns, rural areas, immersive cultural encounters, and destinations off the established circuit. The segment is large, growing, and willing to pay premium prices for experiences that feel genuine.

Africa’s position in this landscape is paradoxical. The continent possesses cultural assets with diverse ethnic traditions, musical heritage, textile crafts, culinary practice, archaeological sites, oral histories, living ceremonial culture, that are precisely what this demand is seeking.

Egypt has successfully commercialised its Pharaonic heritage at scale, with the Grand Egyptian Museum opening in November 2025 reinforcing its position as a global cultural destination. The Maasai communities of East Africa have developed cultural tourism that sustains both income and communal integrity. These are not isolated examples. They are proof that the demand can be met and the economic value can be captured.

Global demand for authentic, immersive cultural experiences is documented, growing, and largely unmet by African destinations.

Image Credit: Euromonitor International Travel Survey

Across most of the continent, cultural experiences remain informally organised, difficult to discover, and inconsistent in quality from a visitor’s perspective. A traveller willing to pay for a two-day immersive craft apprenticeship in a West African textile tradition cannot reliably find, book, or reach it through any platform that meets the expectations shaped by comparable experiences in Southeast Asia or Southern Europe. This is a structural and organizational gap.

Africa does not lack the culture that global demand is seeking. It lacks the packaging, the digital infrastructure, and the service consistency to convert that demand into economic value at scale.

Closing this gap requires three things working simultaneously. Training that equips cultural guides, artisans, and hospitality workers with interpretive skills and service standards, with care taken to ensure it is done without diluting authenticity. Digital infrastructure that allows travellers to discover and book cultural experiences through platforms that meet contemporary expectations. And community-led revenue models that ensure income reaches cultural practitioners directly, creating economic incentives for preservation.

Rural and heritage-based locations across the continent already appear on UN Tourism’s Best Tourism Villages list in recognition that the assets are present and the potential is understood internationally. Yet, it is the ecosystem infrastructure of service reliability, digital discoverability, physical access, trained personnel, that converts potential into performance.

That infrastructure is where the investment gap is most acute, and where it is most consequential.

Destinations like this already meet the conditions global travellers are looking for, but the infrastructure that makes them findable, bookable, and worth the journey does not yet exist at scale.

Image Credit: UN Tourism (2024)

What December’s Developments Tell Us

The three stories in this edition share a structural argument. Makoko is a story about who absorbs the costs of urban development that positions itself as tourism strategy. The domestic revenue data is a story about where tourism income actually comes from, and how misaligned policy investment has been with that reality. The cultural tourism gap is a story about a conversion problem: assets and demand exist on both sides, but the ecosystem infrastructure to connect them does not.

Lagos has a waterfront with genuine cultural and economic value. Africa’s middle class is already travelling and already spending at scale. The continent’s cultural heritage is precisely what the fastest-growing global tourism segments are seeking. The deficit is in the systems, the lack of planning frameworks, investment priorities, policy orientation, that determine whether value is captured broadly or narrowly, durably or not at all.

Tourism policy that focuses on international arrival numbers while underinvesting in domestic infrastructure, informal community integration, and cultural experience packaging is not building a resilient sector. Rather, it is building a sector that performs when conditions are favourable and contracts when they are not. The data from Africa’s strongest tourism economies already shows the alternative. The question is whether the policy follows.

When Growth Meets Affordability: Africa’s Tourism Paradox in December

Reflections on Nigeria’s Detty December pricing issues, continental performance gaps, and the evolving face of wellness tourism.

The 2025 yuletide season highlighted the growing tension between commercial opportunity and cultural sustainability in travel and hospitality in Nigeria. The “Detty December” festive celebration sparked conversations about who gets to party and at what price. The controversy goes beyond simple economics. It touches on questions of cultural ownership, public responsibility, and whether Nigeria’s tourism ambitions align with the realities on the ground.

Across Africa, North African destinations continue to lead in tourism competitiveness, while sub-Saharan nations struggle to transform natural and cultural assets and resources into comparable visitor numbers, mainly due to structural gaps. Globally, wellness tourism is rewriting narratives about who engages more in yoga retreats and mindfulness experiences. Men now make up a fast-growing segment of this market, opening doors for destinations willing to rethink their offerings.

Three forward-looking pointers have emerged:

Key Takeaways

Nigeria’s festive inflation pricing controversy risks alienating the community spirit that led to the organic rise of Detty December. The task ahead? How to balance commercial viability with cultural authenticity and local accessibility when international audiences willing to pay premium prices enter the equation.

Africa’s tourism growth trajectory remains strong, but disparities between North African markets and sub-Saharan destinations are widening, suggesting structural advantages in infrastructure, connectivity, and institutional support that sub-Saharan Africa must address to compete globally.

Wellness tourism is evolving beyond gendered assumptions. The rapid growth of wellness and yoga tourism, particularly among men, signals opportunities for inclusive, experience-led hospitality design across African destinations.

Nigeria’s Detty December: When Commercialization Overshadows Celebration

Lagos in December has become synonymous with parties, concerts, and cultural energy that draws residents in Nigeria as well as Nigerians from the diaspora back home. However, the December 2025 festivities became the subject of widespread social media commentary regarding pricing practices across the hospitality ecosystem, particularly in Lagos. Event ticket prices rose as high as 750 – 1,500 per cent since 2019, far outpacing inflation. Regular tickets to music concerts in December surged as high as ₦75,000–₦150,000, with premium tickets exceeding ₦300,000. The pricing escalation extended beyond events to hotels, self-serviced apartments, bars, lounges, and even e-ride-hailing services, creating a perception of consumer exploitation, rather than market-driven adjustments.

The factors driving this high pricing are complex but not far-fetched. High production costs, artist fees, logistics challenges, and minimal government support for cultural events compel organizers to adopt premium pricing models. The growing diaspora audience (IJGBs), who are attracted to Lagos’ vibrancy in December, are accustomed to international pricing for events and hospitality facilities and services, and have become the major target market for these offerings. This creates an economy where the local purchasing power becomes less relevant compared to the opportunity for service providers to optimize revenues. What emerged from these commentaries was not merely frustration about cost, but concern that a once-communal and affordable celebration is fast transforming into a luxury product accessible primarily to international visitors and the local elite.

Another growing concern lies in the absence of value commensurate with the pricing. Premium pricing requires premium experiences. However, comments on social media also noted that high costs were compounded by inconsistent service quality across the tourism value chain, inadequate facilities, and limited attention to the overall visitor experience. Global tourism trends favor purposeful, experience-driven travel with transparent pricing. When cost exceeds perceived value, visitors may be forced to redirect their attention and spending to destinations offering clearer value propositions. This becomes a dual risk: Detty December then becomes unaffordable for locals, while international visitors conclude that comparable experiences exist elsewhere at better value.

The festive period has concluded, but questions about sustainability remain, as well as the need for stakeholders to return to the drawing board, reflecting on the 2025 Detty December experience, and addressing these gaps for future festive seasons. Can Detty December be transformed from a concentrated moment into a more robust creative and cultural programme for year-round tourism appeal? Can the model extend to other Nigerian cities such as Abuja, Port Harcourt, Ibadan, Calabar, etc., distributing economic benefits beyond Lagos?

The challenge is structural. Cultural capital cannot be monetized without corresponding public investment in infrastructure, security, and destination management. Private operators currently shoulder these burdens while navigating inadequate facilities, complex regulations, and economic volatility. Without coordinated public-private intervention, Detty December risks remaining an extractive annual event that generates short-term gains without building Nigeria’s long-term tourism competitiveness.

Detty December in Lagos has become synonymous with parties, concerts, and cultural energy. But December 2025 left a sour taste, based on social media commentaries.

Image Credit: Wun World Tour (DettyDecFest)

The opportunity for stakeholders is to treat Detty December as the anchor of a year-round cultural calendar, not an isolated peak. Festivals, exhibitions, performances, and other experiences can be spread across months and regions, ensuring that residents and visitors always have something to do and somewhere to visit. Programmes should be inclusive and affordable, so participation is broad and repeated visitation is encouraged. At the heart of this approach is consistent, high-quality service. When service is prioritized, experiences justify their pricing, stakeholders earn sustainable returns, and visitors feel valued, creating a win-win for government, private operators, communities, and the wider tourism economy.

Africa: Divergence Between North and Sub-Saharan Tourism Performance

Africa’s tourism sector recorded a 12 per cent increase in international arrivals in early 2025, outpacing all other global regions and approaching 96 per cent of pre-pandemic revenue levels by 2023. Countries like Morocco, Egypt, Rwanda, and South Africa are leveraging tourism for GDP growth, job creation, and foreign exchange earnings, demonstrating the sector’s potential as an economic development tool.

Morocco, for instance, welcomed a record 19.8 million tourists in 2025, generating US$13.5 billion in revenue. This was driven by expanded flight networks, major cultural attractions, and the hosting of the Africa Cup of Nations (AFCON), the continent’s biggest football tournament. Egypt similarly posted impressive numbers with 19 million visitors, marking a 21 per cent rise attributed partly to the opening of the Grand Egyptian Museum and coordinated government campaigns targeting higher visitor volumes.

Tourism growth in Africa, however, is unevenly distributed. According to the WEF Travel & Tourism Development Index 2024, North Africa consistently outperforms sub-Saharan Africa across nearly all metrics except human resources and labour markets, natural resources, and travel and tourism environmental, socio economic and demand sustainability. This performance gap points to advantages in physical infrastructure, regulatory frameworks, international connectivity, and institutional support that compound over time. Sub-Saharan countries, despite having rich cultural and natural assets, as well as a higher potential for sustainability and demand, struggle with fragmented visa policies, underdeveloped transport corridors, and limited public-private coordination.

This divergence raises critical questions about development pathways, and suggests that tourism success is less about destination appeal and more about systemic enablers, something policymakers, particularly in West and Central Africa, may need to prioritize. The infrastructure deficit is substantial, from airports to urban, rural and regional road networks, to telecommunications, electricity, and other tourist support services and infrastructure. Regulatory environments in many sub-Saharan markets also create friction for both visitors and operators through complex visa regimes, inconsistent policy implementation, and bureaucratic obstacles.

The way forward for policymakers and investors is to address existing gaps through targeted interventions, starting with a clear commitment to recognizing the economic potential of tourism. Strong political will is essential. Rwanda shows that focused investment in specific niches, such as high-end gorilla tourism and MICE travel, can deliver results even in smaller markets. The country earned US$647 million from tourism in 2024 and has been projected to generate over US$700 million in 2025.

South Africa’s tourism has demonstrated what mature infrastructure and consistent, effective marketing can achieve. The country recorded 8.56 million international tourists between January and October 2025, an increase of 1.3 million arrivals compared to the same period in 2024. Kenya and Tanzania are also building strong tourism economies through sustained investment in wildlife conservation, infrastructure, and regional marketing.

In terms of destination competitiveness, North Africa leads across nearly every metric except human resources, labor markets, and natural resources.

Image Credit: Travel and Tourism Development Index 2024 (World Economic Forum)

Other Sub-Saharan African countries can learn from these examples and adapt relevant lessons to their own contexts. Regional bodies like the African Union, the Economic Community of West African States (ECOWAS), and regional economic communities can support coordination on key issues, including visa policies, monitoring the implementation of the AfCFTA agreement, aviation liberalization, and standards harmonization, to strengthen the sector across the continent.

The global yoga tourism market reached US$177.1 billion in 2024, and is projected to grow to US$222.5 billion by 2030, representing a 3.9 per cent compound annual growth rate, according to industry analysis from Research and Markets. This expansion is fueled by demand for experiences combining physical health, mental balance, cultural immersion, and personal transformation. While women continue to dominate participation, men’s engagement is growing rapidly, which can signal opportunities for inclusive wellness packages for Africa.

Yoga and other forms of wellness tourism were traditionally dominated by women, but male participation is growing

Image Credit: Avec Sport

The United States remains the largest market for yoga tourism, while China shows rapid growth trajectory. Other markets demonstrating sustained expansion include Japan, Canada, Germany, and several destinations across Asia-Pacific, Latin America, the Middle East, and Africa. Tourists increasingly seek experiences that go beyond passive recreation, looking instead for activities that deliver measurable improvements in physical fitness, mental clarity, and overall well-being. Corporate wellness programmes have further normalized yoga and mindfulness practices, creating familiarity and demand that extends into leisure travel choices.

The growing male participation in yoga tourism represents a notable cultural shift. Practices historically associated primarily with women are finding broader appeal. This appeal appears tied to several factors: First, elite athletes and sports teams integrate yoga into training regimens for performance optimization, flexibility, and injury prevention. Second, corporate wellness programmes have normalized mindfulness and yoga as tools for productivity, focus, and stress management in high-pressure professional environments. Third, scientific validation of yoga’s benefits for mental health, cognitive function, and physical performance gives the practice credibility beyond spiritual or alternative health contexts.

For African destinations, wellness tourism presents a largely untapped opportunity. The continent’s natural landscapes, cultural diversity, and lower operational costs compared with established markets in Asia and Europe provide competitive advantages. Countries such as Morocco, Kenya, and South Africa have emerging wellness tourism sectors, but inclusive and comprehensive packages remain limited. Integrating yoga, mindfulness, and wellness practices with African cultural experiences, adventure activities, and quality hospitality could create distinctive offerings that attract the growing global wellness tourism market. Realizing this potential requires investment in trained instructors, suitable facilities, well designed programming, targeted marketing, and partnerships with wellness travel platforms and operators.

The combination of wellness tourism with Africa’s natural assets, including beaches, mountains, wildlife reserves, and deserts, allows destinations to offer unique wellness experiences. Well-curated programming can help attract visitors, even during off-peak seasons, diversify revenue streams beyond in-city and traditional destination tourism, and appeal to health-conscious professionals, corporate groups, and solo travelers who are currently underserved in Africa. The continent’s indigenous wellness practices and herbal knowledge can position the continent to capture a meaningful share of this market as wellness tourism continues to expand worldwide.

Implications and Lessons for Stakeholders

Extend Detty December programming beyond Lagos and beyond December. Year-round cultural events across multiple Nigerian cities can reduce the fixation on a single month in one location, regulate seasonal price surges, and build a broader, more sustainable tourism ecosystem.

Target specific infrastructure gaps identified in global competitiveness indices. Sub-Saharan destinations should focus investments on air transport, ICT readiness, visa facilitation, and regional aviation liberalization. These areas yield disproportionate returns in visitor arrivals and economic impact.

Develop locally-rooted wellness packages. African hospitality providers can combine yoga and mindfulness with cultural immersion, adventure activities, and luxury amenities to position Africa competitively against established Asian and European wellness markets.

Prioritize transparent, all-inclusive pricing. Build trust and encourage repeat visitation by eliminating hidden costs and clearly communicating value propositions. This aligns with global consumer preferences for authentic, purposeful travel experiences.

Invest in consistent service quality across the tourism value chain. Premium pricing requires premium experiences. Destinations that consistently deliver value matching or exceeding cost build loyalty, positive word-of-mouth, and long-term competitiveness in an increasingly crowded global tourism market.

Diaspora Investment, Wellness Growth, and Africa’s Emerging Experience Economy

November reflected a tourism landscape in transition. Diaspora backed investment in leisure and hospitality facilities in Nigeria, particularly in Lagos, has increased. Global wellness markets continue to expand, and digital nomadism is reshaping urban hospitality across Africa. These trends raise strategic questions: Can seasonal booms be converted into sustainable, year-round economies? And can African destinations evolve from passive backdrops to intentional, experience-driven wellness economies?

Key Takeaways

Diaspora capital is driving growth in Nigeria’s leisure and hospitality sector, particularly in Lagos, but activity remains highly seasonal.

Reduced outbound education and medical tourism presents a window to upgrade domestic services.

Global trends such as wellness tourism and digital nomadism offer high-value opportunities if infrastructure, regulatory support, and strategic planning align.

Nigeria: Diaspora Investments and Domestic Medical/Educational Tourism Opportunity

Investment in leisure and hospitality in Lagos is expanding, encompassing entertainment facilities, restaurants, bars, lounges, self-serviced apartments, boutique hotels, and small scale resorts. Demand for hospitality facilities and services peak during the Detty December festive season, driven by returning diaspora and local travelers, creating both high revenue potential and intense seasonal pressure.

This growing investor interest is facilitated by Lagos State’s relatively investor-friendly regulatory framework, which has enabled diaspora entrepreneurs to participate in leisure infrastructure development. However, while festive-season peaks generate visibility and short-term gains, sustaining occupancy and revenue during off-peak periods remain a challenge. Outside this window, visitor volumes decline, and within this window, current leisure offerings are mostly targeted towards young adults, nightlife lovers, and the ‘I Just Got Back’ (IJMB) seasonal diaspora returnees in December. The broader question, not just for investors and business owners but also for public-sector stakeholders who create the necessary policy reforms and an enabling environment, is how to convert this episodic end-of-year enthusiasm into more robust, year-round programming and economic activity.

Even more importantly, how can we expand this end-of-year festive culture beyond Lagos and build more intentional programming and infrastructure across multiple states and cities, and position Nigeria as a year-round tourism destination, and not just Lagos as an enclave for Detty December?

For leisure and hospitality in Lagos, and by extension Nigeria, to thrive beyond seasonal surges, they may benefit from diversified programming, such as school excursions, corporate events, or wellness activations, that smooth demand across the calendar year. This will include aligning offerings with the seasons, weather patterns, traveler interests, and key cultural or heritage months, all curated through the lens of local context and community identity. Developing multi-purpose facilities capable of hosting year-round programmes that appeal to people of all ages and backgrounds, as well as improving tourist infrastructure across the country, can also help diversify revenue and justify further investment.

Lagos thrives on “Detty December” buzz, but its leisure economy remains seasonal and appealing to a limited market. Can its nightlife offerings and diaspora energy be turned into year-round appeal?

Image Credit: BBC (The Plug Entertainment)

Africa’s Growing Digital Nomad Market

Urban African destinations are increasingly attractive to global digital nomads, drawn by reliable air connectivity, internet speed, cultural richness, and affordability. Cities like Cape Town, Marrakech, Nairobi, and Egypt’s coastal cities are gaining traction as global digital nomad destinations, offering a mix of connectivity, culture, and cost. Yet most of these remote workers come from outside Africa: Europe, North America, the Middle East, and Asia. Intra-continental mobility for African professionals remains constrained by visa regimes, uneven internet reliability, and limited regional air links.

Seven of the top 10 cities for digital nomads in Africa are in North Africa, with Egypt alone accounting for four. In sub-Saharan Africa, only Senegal represents West Africa, and Kenya represents East Africa. This signals a significant gap and opportunity for other African countries.

Digital nomads need more than reliable internet, seamless travel, and coworking spaces to be drawn to destinations; they are attracted to the authentic culture, lifestyles, and hospitality of the host community. If a destination offers little beyond what they would usually find back home, this would not be a compelling reason for them to travel. To attract this growing market, sub Saharan African cities will need to be more intentional: rather than design foreign hospitality offerings to capture digital nomads, the focus should be on authenticity, affordability, and meaningful immersive experiences.

Of course, it goes without saying that dependable digital infrastructure, tourist service facilities, and improved transport connectivity are non-negotiables.

Beyond this group, there are also African tech workers and entrepreneurs who are able to live and experience different parts of the continent whilst working remotely. Investors can consider creating integrated live-work-play environments in cities, combining coworking spaces, extended-stay accommodations, and affordable and attractive tourism and lifestyle experiences for digital nomads from Africa, not just from outside of Africa. The governments will have a role to play: coordinated and streamlined visa policies, improved internet reliability and digital connectivity, and visitor safety to enable intra-African professional mobility, ensuring that African talent benefits alongside global remote workers.

Digital nomads and remote workers are driving demand for lifestyle-rich destinations across Africa, fueling growth in co working hubs, long-stay housing, and culture-embedded neighbourhoods.

Image Credit: A seaside outdoor restaurant in Cape Town, South Africa (Girl on a Zebra)

Global: The $6.8 Trillion Wellness Economy and Generational Travel Trends

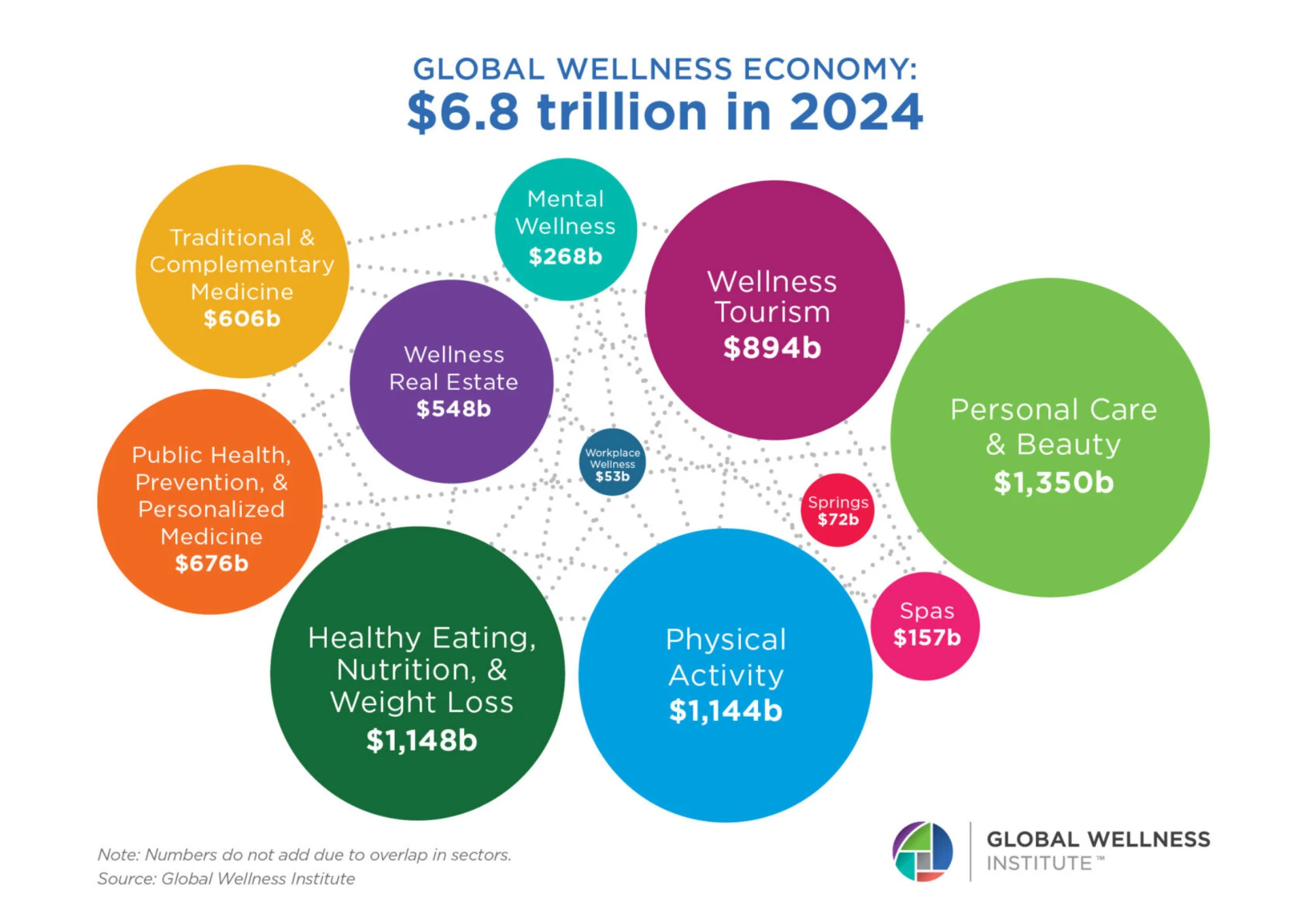

Wellness tourism is no longer an offering for the rich and luxury loving. Global demand for mental wellness, nature immersion, mindfulness retreats, and holistic experiences is surging. The global wellness economy was valued at US$6.8 trillion in 2024 and is projected to reach US$9.8 trillion by 2029, is driving growth in wellness-focused tourism, including spas, retreats, and wellness real estate (Global Wellness Institute, 2025).

Africa’s landscapes, from highland forests to coastal lagoons, offer ideal foundations for purpose-built wellness destinations. Some resorts, however, treat wellness as a secondary amenity rather than a core product. Developing wellness tourism that integrates local healing traditions, herbal and indigenous knowledge, communal wellness practices, and ecological sustainability can differentiate African destinations and their wellness offerings globally. This requires trained practitioners, certification standards, and deliberate infrastructure planning.

The global wellness economy market is projected to grow to as high as US$9.8 trillion by 2029. Africa’s landscapes, wellness practices, and herbal knowledge are suited to tap into this growing market.

Image Credit: Global Wellness Economy Growth Projections from 2013-2029 (Global Wellness Institute)

Digital mobility and changing traveler preferences are also redefining demand: Generational shifts, hybrid work trends, and remote mobility are influencing how, when, and why people travel, creating opportunities for innovative products, infrastructure, and policy interventions. Recent data on European travel patterns (notably France, Germany, and the UK) observed by a study by the European Travel Commission show distinct generational preferences: younger travelers seek affordability and spontaneity; midlife travelers balance work and leisure; older cohorts prioritize comfort, wellness, and cultural enrichment. As Africa’s middle class grows, similar segmentation is likely to emerge.

This is a leading indicator for Africa. As Africa’s middle class grows, similar patterns may begin to emerge. One-size-fits-all tourism products may struggle to retain relevance. Businesses and destinations can key into this growing trend by segmenting their offerings: budget-friendly, experience-rich stays for Gen Z; flexible, mid-tier wellness or cultural packages for Millennials and Gen X; and premium, all-inclusive heritage or nature retreats for older travelers. Tourism operators will need tailored experiences that account for life stage, digital behavior, and spending power. Mobile-first booking, flexible pricing, and curated itineraries will be essential to capture the emerging cross-generational demand effectively.

Implications and Lessons for Stakeholders

De-seasonalize leisure and hospitality investments by designing facilities for multi-purpose use to smooth revenue across the calendar.

Develop wellness tourism as a primary product by integrating local traditions, ecological principles, and global standards to create distinctive, authentic experiences.

Segment tourism products by life stage and digital behavior, using mobile-first platforms to deliver flexible, personalized, and experience-rich offerings.

October reiterated a compelling narrative across tourism markets: Africa is accelerating through cultural capital and conservation-led experiences, even as global pressures such as rising operational costs, climate volatility, and workforce shortages reshape the sector.

For policymakers, investors, and industry stakeholders, here are three (3) key takeaways defining this momentum:

Authenticity is emerging as the new premium: Africa’s competitive edge in tourism continues to lie in its cultural and ecological distinctiveness, from Lagos’s mangroves to South Africa’s design-forward accommodation. The most valuable opportunities are now tied to investments that deepen local identity rather than replicate global templates.

Conservation and culture function as economic infrastructure. Wildlife protection, mangrove restoration, and heritage stewardship are no longer soft concerns. They form the basis of investor confidence, visitor trust, and long-term revenue. When these assets weaken, as seen in Etosha or in the delayed opening of MoWAA, entire tourism economies feel the impact.

Operational resilience must be embedded in strategy. Climate shocks and labour shortages are baseline risks. Sustainable growth requires integrating ecological safeguards and human capital planning into business and policy frameworks. These are not optional add-ons. They influence performance.

Nigeria: Regulation and Cultural Capital

The passage of the Endangered Species Conservation and Protection Bill in October 2025 marks a significant step in positioning Nigeria as a credible steward of biodiversity. With fines of up to ₦12 million, potential jail terms of 10 years, and expanded enforcement powers for Customs, the law aligns Nigeria with global conservation standards. This is especially urgent given the precarious status of Nigeria’s wildlife, some of which are endangered. While exact, up-to-date numbers are difficult to pinpoint, Nigeria has fewer than 300 Cross River gorillas, fewer than 34 West African lions, and fewer than 200 West African forest elephants. Pangolins, manatees, and the African wild donkey are just some of the country’s critically endangered species.

For tourism and hospitality stakeholders, as well as biodiversity conservation enthusiasts, this legal framework will enhance Nigeria’s appeal to environmentally conscious travelers and investors such as the World Wildlife Fund (WWF). The test now lies in consistent field-level implementation. Practical measures such as community monitoring teams, digital tracking tools for wildlife corridors, and routine enforcement reports will strengthen transparency and credibility. Without these, the deterrent value of the law risks remaining theoretical rather than operational.

Lagos’s successful hosting of Africa’s first E1 Electric Powerboat Race in October 2025 demonstrated Nigeria’s capability to host sustainability-focused global events. Beyond its spectacle, the event carried a deeper strategic intent: to spotlight the urgent need for mangrove restoration across West Africa’s coastal region. Over 30 per cent of Nigeria’s mangroves have disappeared in the past three decades due to expansion, pollution, and logging. Ecosystems have been washed away, and livelihoods have been lost.

But recently, hope has begun to take root again: communities in places like Ogoniland are demanding restoration; young mangroves are now being replanted to allow for the full restoration of the environment. The E1 event’s sustainability narrative retains meaning only if it inspires local stewardship. This requires community-led restoration programmes involving fishermen, youth groups, and women’s cooperatives. For investors, it also opens opportunities for mangrove-based ecotourism, for instance, guided kayak trails and environmental education tours that support regeneration.

The Museum of West African Art (MoWAA) stands complete in Benin City, yet remains underutilized due to unresolved disagreements among traditional leaders, government agencies, and cultural custodians.

Image Credit: MoWAA Website

A challenge remains in Benin City, where the dispute surrounding the launch of the Museum of West African Art (MoWAA) has slowed its emergence as a major cultural destination. Although the building is complete, the absence of alignment among traditional institutions, government bodies, and cultural custodians continues to limit public access. The situation illustrates a recurring issue in heritage projects: insufficient early consensus among stakeholders. Broader and early engagement with legitimate stakeholders, anchored in public education and cultural access, may have prevented current tensions. The way forward is collective focus on legacy, shared ownership, and public value.

Africa: Growth in South Africa, Climate Vulnerability in Namibia

South Africa’s hospitality sector is on a robust growth path, with market value expected to rise from US $11.49 billion in 2025 to US $15.64 billion by 2030. Niche, experience-led products such as boutique hotels, serviced apartments, and culturally driven design are driving this expansion. The trend highlights a broader continental opportunity. African hospitality can compete globally by elevating local identity and strengthening operational quality. Investors are already responding to design-led stays that weave in local art, cuisine, and storytelling, proving that “local” can also be premium. Growth will, however, depend on avoiding the dilution of cultural character and ensuring local talent is integrated, trained and upskilled into management and ownership.

Over one-third of Etosha National Park’s habitat was lost to wildfire, threatening a tourism economy that relies on the park for nearly 30% of its revenue.

Image Credit: Elephants drink at a waterhole in Etosha National Park. (AP Photo)

Conversely, Namibia’s recent wildfire in Etosha National Park in September 2025 which destroyed over one-third of its ecosystem, exposed a stark vulnerability. With tourism projected to face a two to three-year recovery period, the incident underscores how climate shocks can rapidly erode natural capital that underpins entire economies. Etosha contributes almost 30 per cent of Namibia’s tourism revenue, which means the impact will stretch across employment, foreign exchange, and conservation financing. The lesson is clear. Conservation tourism cannot rely on reactive protection. Early warning fire systems, rapid-response community teams, diversified water management, and ecological corridors form the foundation of investor confidence and long-term resilience.

Global: Tourism’s Looming Workforce Crisis

The World Travel and Tourism Council’s projection of a 43 million worker shortfall by 2035, despite the sector creating 91 million new jobs, reveals a deep structural mismatch in global labor markets. This is a systemic imbalance driven by aging populations, shifting worker preferences, and accelerating demand that outpaces talent pipelines. The shortfall is most acute in high-growth markets like China and India, where rising middle-class travel and digital-native expectations are increasing pressure on service delivery. Yet many former hospitality workers have not returned, drawn instead to sectors offering better wages, stability, or remote flexibility.

For business leaders in Africa, the response should not be limited to recruiting more to balance the cycle of incoming and outgoing talent in the industry. Sustainable staffing will require redefining the value proposition of working in the hospitality, travel, and tourism industry through competitive compensation, clear career progression paths, and targeted upskilling that elevates roles beyond transactional tasks.

This means aligning training and development with emerging skill demands across roles. At the managerial and executive level, critical thinking and analytical skills are already important, but greater proficiency is needed, especially as creative thinking is expected to grow significantly in relevance. In customer-facing roles, leadership and management capabilities will become increasingly vital, yet current proficiency remains low. For operational roles, reliability and detail orientation, along with flexibility and resilience, are seen as highly important.

Hospitality and tourism businesses in Africa will need to rethink their workforce strategy to address the deepening global talent gap. Offering fair pay, competitive benefits, meaningful career pathways, and role-specific upskilling can position tourism work as purposeful and future-ready. Technology and automation can ease pressure in back-office functions, but frontline experiences will always depend on human connection. The winners will be those who treat workforce investment not as a cost centre, but as a core driver of customer experience and brand resilience.

Excerpt from WTTC Report showing the fastest growing skills, and current most proficient and important skills for managerial and executive level workers in the global tourism industry.

Implications and Lessons for Stakeholders

Stronger conservation laws enhance Nigeria’s eco-tourism positioning, but they require consistent enforcement. Community rangers, digital monitoring, and transparent reporting are essential.

High-profile events such as the E1 Race can drive ecological action. Partnerships with coastal communities will strengthen mangrove restoration and add value to ecotourism offerings.

Cultural projects like MoWAA require early and inclusive alignment to avoid strategic bottlenecks. Shared access, education, and cultural value should guide future decisions.

African hospitality will benefit from locally grounded, premium guest experiences. Scaling must not dilute cultural identity or exclude local professionals.

Climate and workforce risks should be integrated into all investment and operational plans. Adaptation systems, fair compensation, and talent development will determine long term sustainability.

September 2025 underscored a pivotal moment in tourism with strong global demand colliding with systemic challenges in Africa; from regulatory shifts and climate volatility to generational redefinitions of travel itself.

For policymakers and investors navigating this complex terrain, three critical imperatives emerged:

Enhanced air connectivity:driven by strategic route expansions and infrastructure investments;

Regulatory recalibration:particularly around consumer protection and visa policies; and

Evolving travel preferences:shaped by digital fluency, sustainability expectations, and generational values (e.g., Gen Z’s embrace of “glamping,” Millennials’ preference for authentic tent stays, and older cohorts’ shift toward recreational vehicles and all-inclusive packages).

These shifts matter for Nigeria, Africa, and global markets alike because they signal where investment, policy coordination, and consumer spending are headed, and why investors, policymakers, and business leaders need to understand these competitive pressures now.

Nigeria’s aviation sector demonstrated notable strength in September, notably through enhanced air connectivity, despite a turbulent regional environment marked by currency instability, airline liquidity crises in neighbouring markets, climate change, and escalating operational costs across Africa.

Some of these include but are not limited to: prolonged aviation strikes in Kenya (triggered by wage disputes and staffing shortages), erratic weather patterns across East Africa (linked to an intensifying Indian Ocean Dipole causing unseasonal flooding and flight disruptions), and broader economic uncertainty in Francophone West Africa.

Despite these challenges, Nigeria advanced its position as West Africa’s air travel hub through concrete actions:

Air Peace launched three weekly flights on its Abuja–London Heathrow route (operating Fridays, Saturdays, and Sundays), alongside three weekly Abuja–London Gatwick services (Tuesdays, Wednesdays, and Thursdays) beginning in late October. This milestone represents Nigeria’s first direct service from Abuja to both major London airports.

The Gateway International Airport in Ogun State commenced operations, positioning Nigeria to decongest Lagos and attract transit traffic.

Air Tanzania introduced a new direct service between Dar es Salaam, Tanzania , and Lagos in September, signaling growing bilateral aviation cooperation.

Intra-Africa air connectivity is expanding, with new routes linking Lagos and Abuja to East Africa, including Lagos to Dar es Salaam, as well as direct flights from Abuja to London’s Heathrow and Gatwick airports.

This momentum was matched by regulatory recalibration: the Nigerian Civil Aviation Authority (NCAA) reported ₦257 million in passenger refunds from January to August 2025, a 137 per cent year-on-year increase, reflecting stricter refund compliance, enforcement of airline accountability, and consumer protection standards. This shift is critical to rebuilding traveler and investor confidence in a market long plagued by service unreliability.

Africa: Policy Boldness vs. Systemic Fragility

Across the continent, September revealed a stark duality. On one hand, policy ambition is accelerating regional integration. Burkina Faso, under President Ibrahim Traoré’s pan-Africanist agenda, waived visa requirements for all African nationals, a bold step aligning with his broader vision of continental unity, economic self-reliance, and resistance to external influence. Similarly, Zimbabwe expanded air routes, including new connections to South Africa and Ethiopia, aiming to revive its tourism economy.

On the other hand, structural vulnerabilities persist:

Aviation strikes in Kenya, caused by unresolved labor disputes over wage arrears, pay and working conditions, as well as staff shortages, disrupted thousands of passengers.

Erratic weather systems in East Africa, driven by climate anomalies, grounded flights and damaged tourism infrastructure, and disrupting flights, wildlife movements, and peak-season planning.

Limited crisis-response capacity in several countries exposed gaps in climate-resilient planning and workforce stability.

These developments underscore the continent’s structural weak points: labour instability, climate risk exposure, and limited redundancy in aviation and tourism infrastructure. The lesson is clear: connectivity alone is insufficient. Sustainable tourism growth in Africa demands integrated strategies that couple open skies with climate adaptation, labor harmony, and digital readiness.

Global Tourism: Strong Demand, Shifting Traveler Preferences

Globally, travel demand remains robust. According to the UN Tourism Barometer, 690 million international arrivals were recorded in the first half of 2025, 33 million more than in 2024. Africa led global growth at 12 per cent, driven primarily by Egypt, Morocco, Kenya and South Africa, which saw strong recovery in both inbound leisure and diaspora travel.

The Middle East (and North Africa (MENA), particularly Egypt, Saudi Arabia, the UAE, and Qatar, continued to outperform pre-pandemic levels, mainly due to increasing Chinese outbound travel, though growth slowed marginally by 4 per cent, likely due to global economic caution and shifting corporate travel budgets. Global tourism is expected to grow by 3–5 per cent in 2025, with France, Japan, the UK, Spain, and Türkiye projected to generate the strongest demand. This growth will be driven by rising middle-class incomes, continued

pent-up interest in travel, and the expansion of low-cost airlines. France and Spain continue to hold their position as the world’s most visited destinations.

Excerpt from the UN Tourism Barometer showing international tourist arrivals by sub-regions from 2019 to 2024, as well as 2025 monthly and quarterly data up until June 2025

Consumer shifts are equally revealing. In RMS’ State of Outdoor Hospitality Report for 2025, the camping and outdoor-stays segment continues to diversify: yurts, domes, and treehouses each hold 29 per cent of the “luxury outdoor stay” market, rivaling traditional tents. This reflects a broader “rewilding” trend, where travelers seek immersion in nature without sacrificing comfort. A September 2025 TravelDaily survey of UK travelers confirmed this cross-generational appeal, amplified by technology: 64 per cent of all bookings are now made via mobile, driven by demand for real-time pricing, flexible cancellations, and integrated reviews.

Image Credit: Pictures of tents in upper collage are from 2025 State of the Outdoor Hospitality Report (RMS); yurts from Musab (Pexels); treehouse from Brett Sayles (Pexels)

Globally, travelers are favouring outdoor stays and experiences (in yurts, tents, caravans and treehouses) across all ages. However, generational differences are defining their outdoor preferences.

Generational differences further segment the market:

Gen Z favors glamping, prioritizing spontaneity and Instagrammable moments.

Millennials still lean toward tent camping but demand eco-certifications and local experiences.

Gen X and Boomers increasingly choose recreational vehicles (RVs) for multi-generational trips, valuing privacy and self-sufficiency.

Yet all groups show rising interest in all-inclusive outdoor packages, as economic uncertainty makes bundled, hassle-free itineraries more appealing.

This momentum is already visible in Africa’s global standing. According to Business Insider Africa (2024), five African countries rank among the world’s top 10 camping destinations: Tanzania (3rd), Kenya (4th), Namibia (5th), South Africa (6th), and Ethiopia (8th). Their success

stems from combining iconic landscapes with well-managed access, conservation integrity, and authentic local engagement.

Top 5 African Countries for Camping Destinations

For hospitality investors across the continent, the message is clear: the next frontier of hospitality may lie beyond conventional hotel lobbies, but in outdoor stays and experiences. Natural assets in Africa (our forests, hillsides, rivers, beaches and even open countrysides), offer opportunities for curated, low-impact outdoor stays. These could include elevated glamping, cultural eco-cabins, or guided wilderness retreats, all supported by intentional safety systems: environmental safeguards, health protocols, and visitor security measures that ensure both guest confidence and ecological protection.

Local communities can anchor this model by co-managing sites, offering guided experiences, preparing traditional meals, or crafting amenities, thereby turning cultural knowledge into economic opportunity.

Strategic Imperatives for 2025 and Beyond

As we move into the final quarter of 2025, the lessons from September are clear.

For Nigeria and Africa:

Leverage aviation momentum with consistent regulatory enforcement and diaspora-focused connectivity.

Address international perception gaps (e.g., Qatar’s visa policy) through diplomatic engagement and traveler education.

Balance policy ambition with investment in climate-resilient tourism infrastructure and labor stability mechanisms. Regional integration must include crisis response protocols.

Countries in Africa that strengthen consumer protections, invest in climate-resilient aviation and tourism infrastructure, and respond quickly to evolving traveller expectations will gain competitive advantage.

For the global industry:

Travel, hospitality and tourism experiences and products should be designed to accommodate generational nuances and digital technology.

Offerings should be anchored in authentic, nature-connected experiences. The future belongs to brands and destinations that combine flexibility, sustainability, and emotional resonance.

Stakeholders across the tourism ecosystem, from policymakers to investors, will need to prioritize strategic foresight, flexible regulation, and experience-driven product development. As global travel continues to rebound, destinations and businesses that succeed will be those that anticipate how regulation, technology, climate pressures, and cultural shifts intersect, and respond with timely, decisive action.

Something transformative happens when industry leaders gather to solve problems together. Much more powerful than networking or knowledge sharing, is the form of collective intelligence that emerges, to truly move the needle forward in developing tourism that actually works for Africa.

Industry leadership goes beyond individual expertise or organizational success. It emerges when experienced practitioners, visionary thinkers, and passionate advocates create space to collectively address the challenges that no single organization can solve alone.

One thing is clear: Africa’s tourism potential cannot be unlocked by an individual or organization alone. It requires a cross-sectoral collective mission. When the industry improves for all, it results in immense returns for the ecosystem, and this includes the organizations and the individuals who work within it.

Our Test Case: The West Africa Tourism Roundtable

Red Clay is proud to have convened the West Africa Tourism Roundtable series as our test case for this principle. Hosted by our venue partners, Radisson Blu Anchorage on Victoria Island, we brought together hoteliers, tourism professionals, destination managers, entrepreneurs, and policymakers, demonstrating this approach in action. The success of these sessions owes much to Radisson Blu Anchorage’s exceptional hospitality and commitment to supporting industry dialogue.

Four years later, we are still receiving testimonials about the partnerships, collaborations and projects that emerged from those sessions. People still ask: “When is the next roundtable?”

The answer lies in understanding why convening matters, and the importance of bringing the right voices together around the right challenges at the right time.

The Magic of Sustained Focus

The West Africa Tourism Roundtable Series featured global industry leaders and practitioners, coming together with a clear objective, to unpack elements of tourism in post-COVID Africa, understanding that the recovery our industry needed, required a form of collective intelligence, to learn from others and to brainstorm on possibilities for the industry of the future.

Over five sessions in the course of one year (ambitious goal!), we were able to truly have sustained focus over a period of time that allowed participants to build on previous discussions, deepen relationships, and develop sophisticated approaches to complex challenges.

A cross-section of the speakers at the West Africa Tourism Roundtable Top L-R: Anita Mendiratta, Dr Belinda Nwosu, Brian Efa; Bottom L-R: Daniel Gray Mwanza, Joel Omeike, Kojo Bentum-Williams

For us at Red Clay, the magic came from the themes that kept coming to the surface over time, showing the interconnected nature of the issues and the need for a systemic approach to addressing the bottlenecks that impede tourism’s progress on the continent.

The top three themes?

The need for accurate data, a truly enabling business environment and patient capital for long-term investment in human capital and the destinations.

Without reliable tourism statistics, policymakers cannot plan effectively, investors cannot assess opportunities properly, and practitioners cannot measure progress meaningfully.

Regulatory frameworks, visa policies, infrastructure, business registration process, all require a cohesive and coordinated approach from policy makers to ensure tourism enterprises are able to thrive, and not merely survive.

Long-term investment is key to a sustainable tourism growth strategy. Tourism is ultimately a people business, and destinations succeed when they invest consistently in capacity building over time.

The Sessions:

Each session built on the previous ones, creating a comprehensive exploration of West Africa’s tourism landscape from multiple angles.

Session 1: Domestic Tourism and COVID-19 Trends and paths to sustainable hospitality, travel and tourism business in West Africa Speakers: Dr. Adun Okupe, Kojo Bentum-Williams, Moyo Ogunseinde

Session 2: AfCFTA and Tourism Entrepreneurship Lessons from the field in West Africa Speakers: Dr. Belinda Nwosu, Daniel Gray Mwanza, Sirili Akko

Session 3: Health, Safety and Security Destination Competitiveness in West Africa Speakers: Dr. Tagbo Azubuike, Anita Mendiratta

Session 4: Sustainability in Tourism How can sustainability thinking become more relevant in tourism development in West Africa? Speakers: Paul Onwuanibe, Joel Omeike, Olivia Ruggles-Brise

Session 5: Hospitality and Tourism Trends Projections for 2022 in West Africa Speakers: Damilola Sobo-Smith, Brian Efa

A cross-section of the speakers at the West Africa Tourism Roundtable Top L-R: Olivia Ruggles-Brise, Paul Onwuanibe, Sirili Akko; Bottom L-R: Damilola Sobo-Smith, Moyo Ogunseinde, Dr. Tagbo Azubuike

The Lasting Impact: One Conversation, One Collaboration at a Time

The true measure of successful convening goes beyond what happens during the sessions: it really is about what happens afterwards.

The West Africa Tourism Roundtable has delivered on this measure in remarkable ways, proving that building tourism that works for Africa happens one conversation and one collaboration at a time.